After several months of very intense and at times chaotic negotiations, the French government has finally managed to get the 2026 budget back on track. Nevertheless, some experts and businessmen believe that this achievement has come at a very high price. Although the new budget is set to decrease the French public deficit from 5.4% of GDP in 2025 to 5% in 2026, it fails to meet the 4.6% target that was initially set by former Prime Minister Francois Bayrou.

However, observers have warned that this deficit could put France behind its commitment to reduce the deficit to 3% by 2029 in the European Union. The country’s public debt has also been on the rise, surpassing 115% of GDP.

How Did the Government Navigate Political Fragmentation?

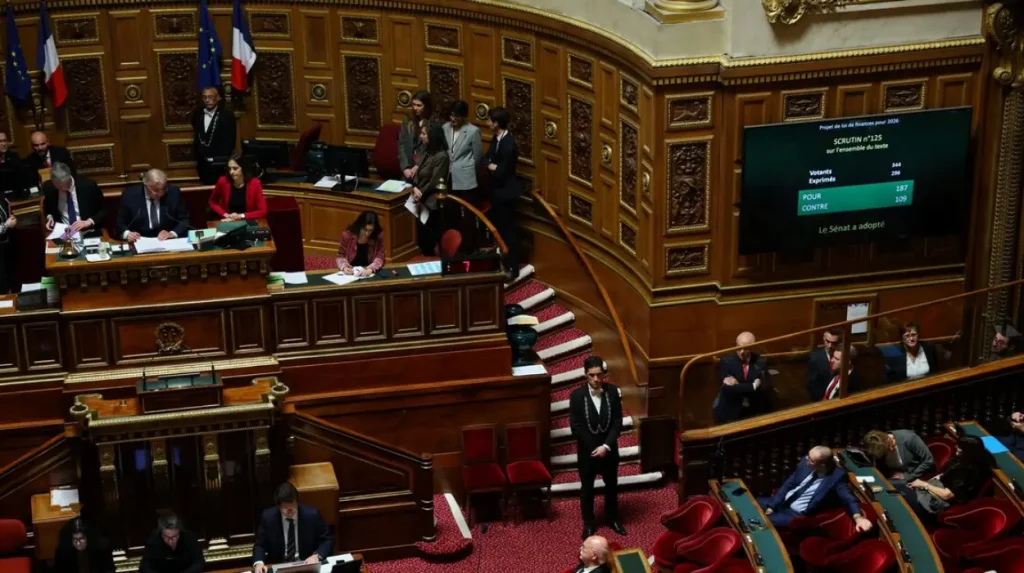

The passage of the budget bill is also significant in terms of the political balancing act that is required in the fragmented parliamentary setting in France. Prime Minister Sebastien Lecornu, who belongs to the centrist party Renaissance, took over a coalition that had lost its majority in parliament following the 2022 election and further lost this majority in a snap election in 2024. In order to manage the situation, Lecornu obtained the tacit support of the Socialist Party (PS) in exchange for a number of concessions, including those that would benefit left-wing priorities.

Lecornu survived two confidence votes after invoking a special constitutional tool to advance the budget without a full parliamentary vote. Announcing the successful passage of the budget on the social media platform X, he wrote:

“France finally has a budget,”

reflecting both relief and the reality that the compromise was born more of necessity than strategic economic vision.

What Are the Implications for France’s Deficit and Debt Targets?

Although the budget makes a small step towards reducing the deficit, it puts France on the wrong track regarding its fulfillment of its fiscal commitments in the long run. As the deficit is estimated to be 5% of GDP, France is still a long way from achieving the target of 3% set by the EU by 2029. This has caused concern among economists that the current path may worsen the debt position of France, which is already over 115% of GDP.

How Does the Budget Affect Corporations and Investment?

The 2026 budget introduces significant changes to corporate taxation that have sparked concern among France’s largest companies. Companies with annual turnover exceeding €1.5 billion ($1.7 billion) face a 20% increase in corporate taxes, while those generating more than €3 billion in revenue are hit with a 41% hike. The government also postponed planned reductions in production taxes, measures initially intended to support corporate competitiveness.

Philippe Crevel, an economist at the Paris-based think tank Cercle de L’Epargne, emphasizes that these concessions are part of the overall compromise with the Socialist Party. Crevel explains that although the left-wing parties were successful in their demands for inflation-adjusted tax brackets, increased top-ups for low-paid workers, and the postponement of the disputed pension reform, Macron’s government maintains essential components of its pro-business agenda. Crevel explains that policies such as the 30% flat tax on investment income and the inability of the Socialists to introduce a 2% tax on the super-rich maintain the economic agenda of the president.

Is Macron’s Pro-Business Record Still Evident?

According to experts, although there have been some left-leaning concessions, it is still possible to notice the pro-business legacy left by Macron. Anne-Sophie Alsif, the chief economist at BDO, points out that, although the government has been struggling to implement further pro-business policies since Macron’s re-election in 2022, the policies adopted during his first term, such as reduced corporate taxes, still contribute to the positive impact.

Alsif points out the most important signs of this heritage:

“Unemployment is down from over 9% to under 8%, France has retained its lead as the top destination for foreign direct investment in Europe for the sixth consecutive year, and re-industrialization projects are underway.”

Alsif considers the 2026 budget to be a “necessary compromise” and points out that the first version of the budget was much more left-wing. The adoption of the budget has already had a positive effect on the markets, as shown by the decrease in interest rates for French 10-year government bonds. Alsif believes that the budget will have a positive effect on GDP growth, which is expected to be around 1% this year.

Why Are Businesses Critical of the Process?

While economists acknowledge the benefits of finally having a budget, business leaders are vocally critical of both the process and its outcomes. Eric Maumy, head of Lyon-based insurance firm APRIL, describes the months of budget negotiations as a “pathetic spectacle” that exposed France to international scrutiny in a negative light.

Maumy, together with about 2,000 other small and medium business owners, founded the movement “Trop, c’est trop” (Enough is Enough) in November 2025, during the peak of the budget crisis. Maumy is critical of the government’s policy of freezing pension reforms, keeping high business taxes, and increasing public spending even further, despite the fact that public spending is already at 57% of GDP.

Is Macron’s Supply-Side Approach in Crisis?

Some economists argue that the 2026 budget marks the end of Macron’s supply-side economic model. Marc Touati, economic adviser at Israel-based investment company eToro, warns that the additional corporate charges will affect the 8.1 million employees of France’s 300 largest companies and their numerous suppliers. He predicts reduced corporate investment, layoffs, and broader economic repercussions.

Touati highlights that Macron’s growth strategy—largely dependent on public spending rather than structural pro-business reforms—has struggled, evidenced by sluggish GDP growth, rising bankruptcies, and escalating public debt from €2.2 trillion in 2017 to over €3.3 trillion today. He cautions that should rating agencies respond negatively, investor confidence could erode, triggering recession and public unrest. Touati asserts that restoring economic stability will require radical corporate tax cuts to re-align France with a genuine supply-side growth model.

What Alternatives Exist for Reviving Growth?

Henri Sterdyniak, economist and founder of the left-wing collective “Les économistes atterrés,” concurs that the 2026 budget represents a pivot away from Macron’s initial pro-business agenda. Sterdyniak critiques the belief that reducing taxes on companies and the wealthy alone would drive substantial investment and employment growth, noting the approach has largely failed to produce its intended effects.

Instead, Sterdyniak advocates a Keynesian strategy, emphasizing massive productive investment across both private and public sectors. He stresses that public debt could be reduced through targeted taxation on the wealthy, including pensioners and higher inheritance taxes. This approach, he argues, could rejuvenate economic growth while ensuring social equity, offering an alternative to the government’s current compromise-driven policy.